The capitalization method of valuation determines the present value of all future income and benefits expected from an investment property from period 0 (today) to perpetuity. However, for many valuations it is necessary to determine the value of an income stream for a period less than perpetuity and compound formulae are used for such valuations.

For example, to determine:

the present and future value of an income stream for a period less than perpetuity: PVPMT, FVPMT.

the rental or annual equivalents of a lump sum payment: PMT

the present or future value of a lump sum: FV, PV.

Here we are concerned with lump sum or single amounts only (FV and PV). The notation used is that for financial calculators and computer spreadsheets. The appropriate keys on a financial calculator are as follows:

FINANCIAL CALCULATOR

N = number of periods (eg number of years)

i = interest rate as a % far the period used in n

PV = present value of a future amount or income stream

PMT = payment or periodic income or outgoing

FV = future value of "amount" of a present amount or future income stream

USING THE FINANCIAL CALCULATOR

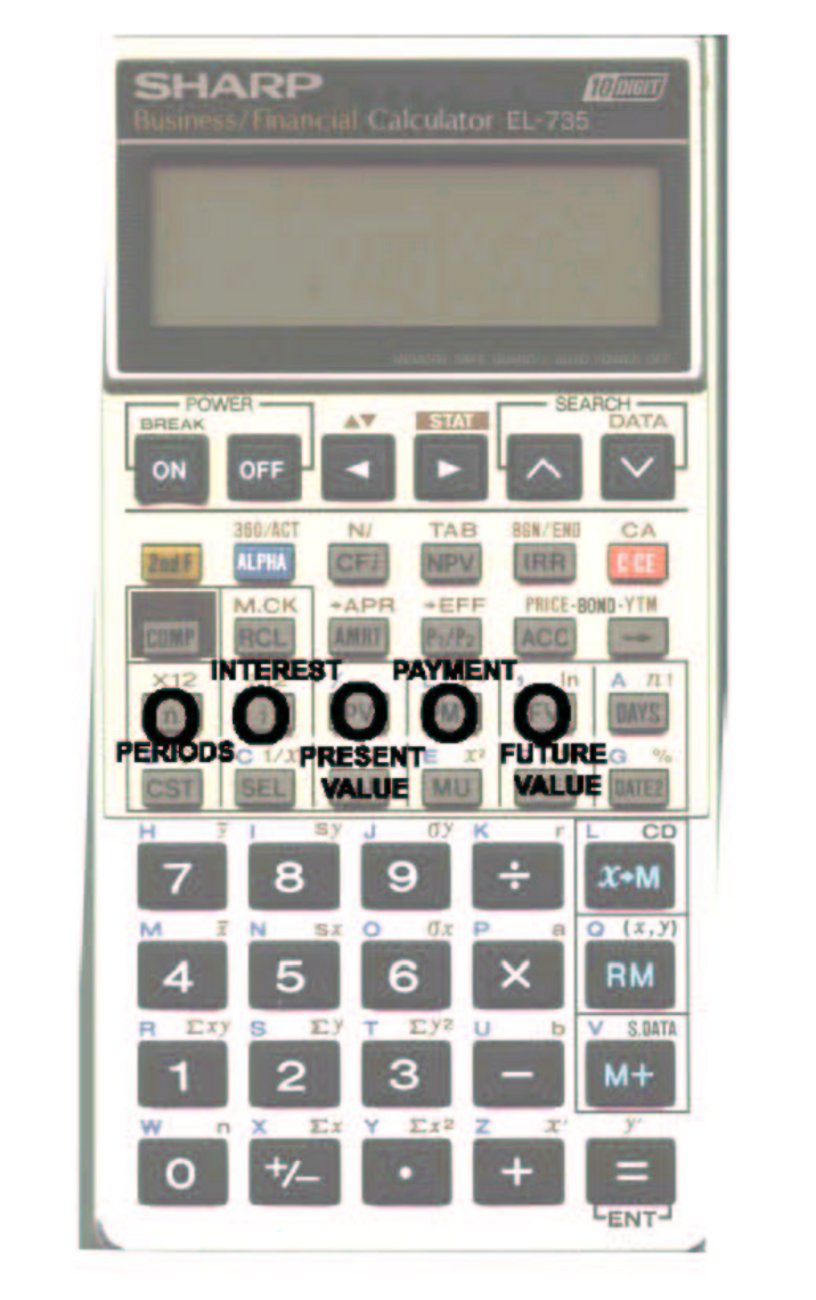

With the above 5 keys almost all financial valuation problems requiring compound functions can be solved. A typical financial calculator is the Sharp EL 735.

DIAGRAM OF SHARP EL 735

The following keystrokes are for the Sharp EL 735 calculator however, most financial calculators have similar keystrokes.

STARTING

The calculator must be in FINANCIAL MODE. The EL735 has a STATISTICAL and a FINANCIAL MODE.

FINANCIAL MODE

The secondary function key = 2nd F.

<2nd F> ( 2nd F will show in display) <STAT>

The calculator can be toggled between the statistical (STAT) and financial modes.

DETERMINING THE AMOUNT OR FUTURE VALUE

STEP 1:

Determine the base (b) with the following formula:

b = 1 +(i/100)

Where:

i = interest rate as a %

EXAMPLE:

b for 12% = 1 + (12/100) = 1.12

STEP 2:

The future value in 5 years at 12% pa Is found with the following formula:

FV = bn

Where:

n = number of years (periods)

b = base

EXAMPLE

The future value of $100 in 5 years time at 12% pa:

B = 1+0.12 = 1.12

FV = 1.125 = 1.7623

The amount of $100 if invested at 12% pa over 5 years will amount to:

$100*1.762 = $176.2

The future value of $176.2 includes interest accumulating at compound rats as shown below:

COMPOUNDING INTEREST at 12% per annum

|

YEAR |

INTEREST |

PRINCIPAL |

|

0 |

|

$100 |

|

1 $100 * 12% |

$12.00 |

$112 |

|

2$112 * 12% |

$13.44 |

$125.44 |

|

3. $125.44* 12% |

$15.05 |

$140.49 |

|

4 $140.49 * 12% |

=$16.86 |

$157.35 |

|

5 $157.35 *12% |

=$18.88 |

$176.23 |

This can be shown on a time scale as follows:

100 112 125.44 140.49 157.35 176.23

=================================>

0

1

2

3

4 5

years

USING THE FINANCIAL CALCULATOR

CLEAR ALL REGISTERS

Modern calculators keep numbers in memory even after the calculator is turned off. Therefore, to make sure all financial memories are clear:

<2nd F><CA> (CA will flash in the window)

DETERMINE THE FUTURE VALUE (FV) OF AN AMOUNT

Enter period: 5 n (n = will show in the window)

Enter interest rate: 12i (i= will show in the window)

Enter present value

(principal): 100 PV

(PV= will show in the window)

NB: 3 inputs of the financial equation are required to calculate the answer to a financial problem:

<COMP><FV> = 176.23

NB: if you do not get this answer try 0PMT then <COMP><FV>

The calculator assumes that any present value is a cost (eg the initial purchase price) and therefore shows the final answer as a negative. In this case, the negative sign is ignored.

The amount or future value that 100 will amount to over 5 years if invested at 12% per annum is 176.23.

See compound functions - spreadsheets

PRESENT VALUE

From the above time scale it can be seen that the present value (PV) of $176.23 in 5 years time is $100. That is, an investor will pay $100 today for the right to receive $176.23 in 5 years time if he/she considers that 12% pa is sufficient return on that investment. Therefore, the investor will pay $1 for the right to receive $1.7623 in 5 years.

How much will he/she pay to receive $1 in 5 years time at 12% pa?

Using ratios from the above time line:

x:1 = 1:1.762

x = 1/1.762 = 0.5674

Therefore, the PV factor for $1 = 1/FV.

Therefore:

PV = 1/FV = 1/ (1.125) = 1/1.762

= 0.5674

The present value factor must always be less than $1 and the future value factor more than $1. The calculation of future or present value of 1 is called a factor because it is the basic value using $1 and the multiplier for finding the value of various amounts.

EXAMPLE

Determine the present value of $1 200 000 due in 5 years at 12% pa:

ANSWER

0.5674 * 1 200 000 = $680 880

The determination of a present value for a future amount is a common valuation problem.

ACCURACY

How accurate should the input data and final valuation be?

It is common to "round off' the final value with a "say" statement. For example:

EXAMPLE

If the final calculation is $680 880 the market value is; say $681 000.

ACCURACY RULES

The following are useful accuracy rules:

INPUT DATA: at least 4 significant figures

FINAL ANSWER: 3 significant figures

EXAMPLE

If answer is $123 344 then say $123 000

USING THE FINANCIAL CALCULATOR TO FIND THE PRESENT VALUE

What is the present value of $8 000 due in 10 years time at 9% per annum?

INPUTS: 10n 9i 8000FV

ANSWER: <COMP><PV> 3379.29

Therefore, the present value of $8 000 in 10 years time at 9% per annum = $3 379.29 say $3 380.

NOMINAL AND EFFECTIVE INTEREST RATES

Banks and financiers commonly quote interest rates as annual nominal rates. For example, 12% per annum nominal.

Nominal in this context means "not exactly". Therefore, when the valuer analyzes the rate for comparison purposes it has to be adjusted to the real or effective interest rate.

If interest is paid monthly, the effective rate =12/12 or 1 % per month.

How

is this amount converted to an annual equivalent?

CONVERSION TO AN ANNUAL EQUIVALENT RATE

The effective interest rate is exactly that amount of interest that $100 will earn over one year. Therefore, to convert a nominal rate to an effective rate the valuer need only calculate how much $100 will amount to over 12 months and then deduct the principal of $100.

EXAMPLE

Determine the effective annual rate for 12% per annum payable monthly.

The amount must be more than 12% because the monthly interest amounts will attract compound interest over the 12 month period.

STEP 1:

b = 1 + 1% = 1.01

STEP 2:

If we invest $100 for 12 months it will amount to:

FV = $100*(1.01)12 = $112.68

STEP 3:

Deduct principal

$112.68 - 100 = 12.68

Therefore, the annual effective rate is 12.68% per annum.

The effective annual rate of 12.68%pa can be used directly in a valuation by capitalizing at the effective rate, annual income but payable monthly.

EXAMPLE

If the present value of the monthly income being received from an investment property is $10 000 per annum then the market value of the property using a capitalization rate of 1% per month (12% nominal) is:

Market value = 100 000 * 100/112.68 = $788 644

say $789 000

TABLE OF COMMON EFFECTIVE RATES OF INTEREST

|

|

EFFECTIVE RATE % PA |

||

|

NOMINAL RATE % PA |

MONTHLY |

QUARTERLY |

HALF YEARLY |

|

4 |

4.07 |

4.06 |

4.04 |

|

5 |

5.12 |

5.09 |

5.06 |

|

6 |

6.17 |

6.14 |

6.09 |

|

7 |

7.23 |

7.19 |

7.12 |

|

8 |

8.30 |

8.24 |

8.16 |

|

9 |

9.38 |

9.31 |

9.20 |

|

10 |

10.47 |

10.38 |

10.25 |

|

11 |

11.57 |

11.46 |

11.30 |

|

12 |

12.68 |

12.55 |

12.36 |

|

13 |

13.80 |

13.65 |

13.42 |

|

14 |

14.93 |

14.75 |

14.49 |

|

15 |

16.08 |

15.87 |

15.56 |

|

16 |

17.23 |

16.99 |

16.64 |

|

17 |

18.39 |

18.11 |

17.72 |

USING THE FINANCIAL CALCULATOR

IF YOU ARE GETTING THE WRONG ANSWER

If all the inputs are correct and you are still getting the wrong answer it is because you have other data in the financial memories:

Clear ALL with <2nd F><CA> or input 0 in those financial keys you are not using.

In the above example: 0 PMT

CHECKING INPUTS

Inputs can be checked as follows for the example above:

<RCL><n> = 10

<RCL><i> = 9

<RCL> <FV> = 8000

<RCL><PV> = 3379.29